Study: Information Desert Leaves Many Suppliers in EV Dust Bowl

The 23rd annual OEM-supplier Working Relations Index (WRI) study finds that suppliers aren’t getting enough insight into automakers’ EV transition plans.

Inadequate information about domestic and Japanese automakers’ product timelines and strategic plans relating to the transition from ICE-powered vehicles to EVs has emerged as a major issue for suppliers, according to an annual study focused on the OEM-supplier working relationship. “The most significant risk of not having a clear roadmap is that it can freeze the supplier,” Dave Andrea, principal in Plante Moran’s Strategy and Automotive & Mobility Consulting Practice, said about his firm’s 2023 North American Automotive OEM-Tier 1 Supplier Working Relations Index (WRI) study.

For many suppliers, it isn’t feasible to simultaneously invest in ICE-related technologies and EV programs. “If they don’t know what to invest in, or when, or how much, they won’t invest in EV programs, as no company wants stranded assets, like a plant standing idle just waiting for an EV program to come to fruition,” Andrea told SAE Media. The most likely outcome from an EV information ‘desert:’ suppliers will continue to focus on existing ICE production orders and investments — as that’s the known revenue source.

“OEMs and suppliers must focus on defining the long-term EV strategy,” said Andrea. In the meantime, suppliers are dealing with many financial headaches, including supply-chain disruptions, soaring raw-material prices and inflationary costs. “Unanticipated inflation has spilled over to labor, transportation, energy and other inputs, and this industry isn’t strong at managing these issues,” Andrea said.

Navigating the ICE-EV transition

While the legacy automakers are supporting their march to electrification with ICE-powered vehicle sales, suppliers essentially are left in a state of flux. “Private-equity firms are looking to consolidate some sectors to keep volumes and scales up in traditional ICE sectors,” said Andrea. Many large suppliers are carving out their pure ICE products and divisions to focus their investments on EVs. Other suppliers are making minimal EV-related investments and/or re-shuffling their product mix.

The number of component providers is expected to decline as the EV transition unfolds. “There will be mergers and acquisitions as companies, particularly in the ICE powertrain area, are de-sourced and revenues go down, making consolidation attractive,” Andrea concluded. For companies producing EV components, the firms unable to grow resources fast enough are likely to acquire technologies as well as add workers and production capacity via mergers or acquisitions.

The WRI study, based on online responses collected from mid-February to mid-April 2023, reflects input from 715 salespeople at 459 Tier 1 companies. The survey addresses suppliers’ perceptions of their relationships with Ford, General Motors, Honda, Nissan, Stellantis, and Toyota. Respondent firms, accounting for approximately 50% of the six OEM’s annual purchases, represent 38 of the Top 50 North American suppliers. Now in its 23rd year, the WRI study was founded in 2001 by Dr. John Henke of Planning Perspectives, Inc. and acquired by Plante Moran in 2019.

Value of communications

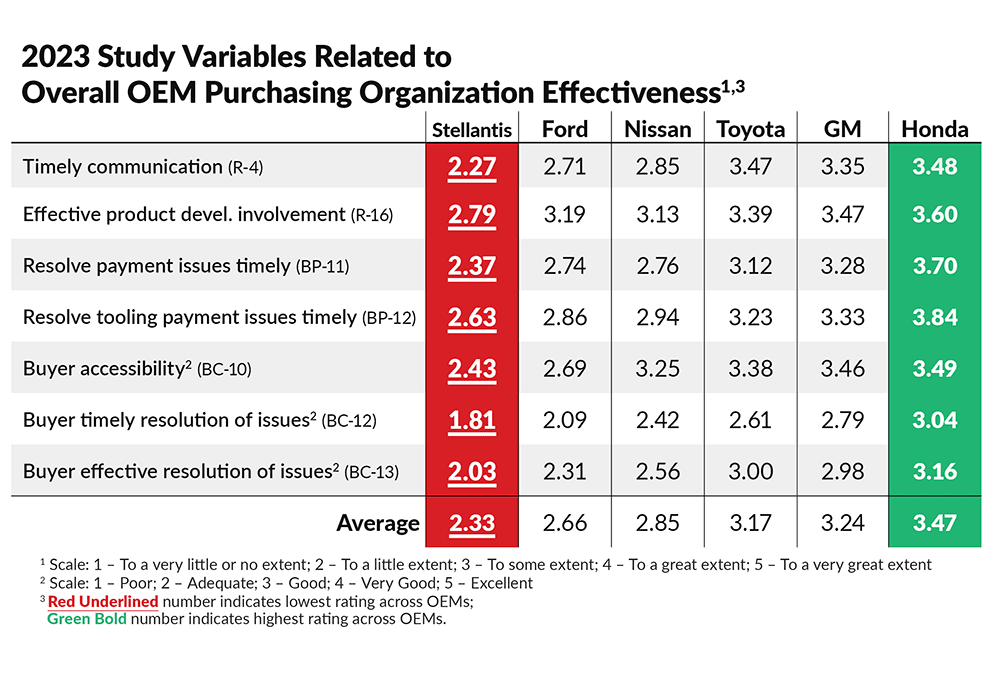

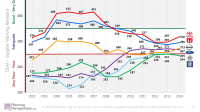

The respected WRI study has repeatedly shown that timely communication and effective product-development involvement are cornerstones to good working relations. “When we ask suppliers which OEMs engage the suppliers most effectively in the product development process, the best-to-last order is Honda, GM, Toyota, Ford, Nissan and Stellantis. “The challenge for automakers is balancing cost competitiveness with strong supplier partnerships by identifying lead suppliers on platforms early,” Andrea said.

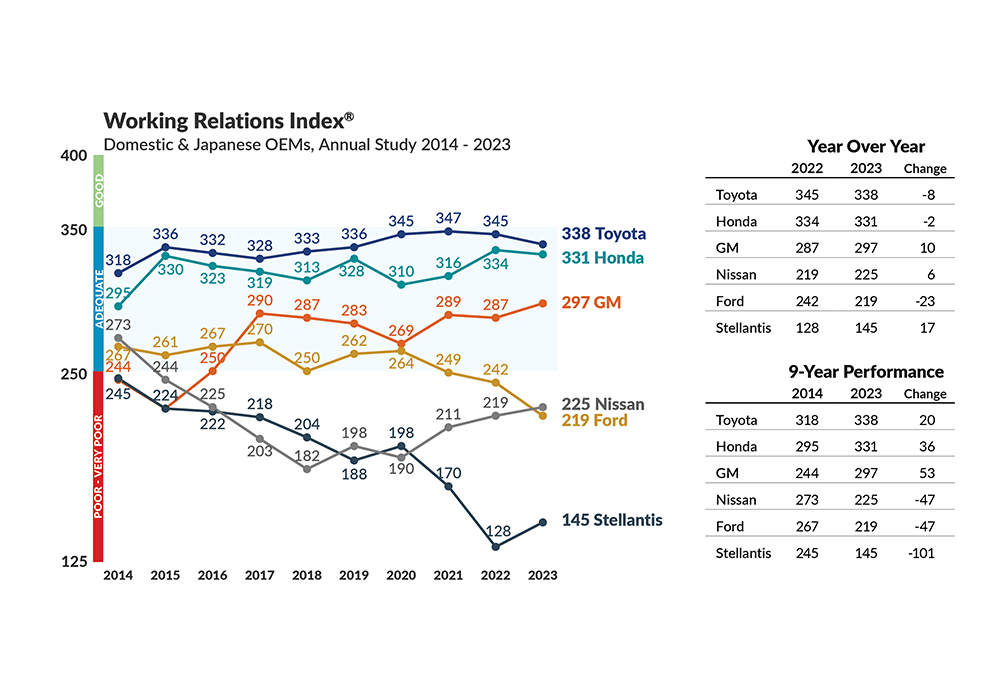

For a record 13th time, Toyota ranked tops in the annual study, followed in order by Honda, GM, Nissan, Ford, and Stellantis. WRI scores dropped slightly for Toyota and Honda. Ford’s scores dipped significantly, while GM, Nissan, and Stellantis improved.

Stellantis had the biggest gain year-over-year, going from 128 to 145 points. “Stellantis’ 17-point increase was driven by a leadership change that reoriented their practices toward building partnerships,” noted Andrea. The 23-point decline for Ford is attributed to organizational moves. “The changes were done to deliver more EV nameplates and production volume, but the transition left suppliers concerned about their long-term future with Ford,” Andrea said.

The biggest surprise of this year’s WRI study was Toyota. “This automaker is known for its continuous-improvement mantra, yet Toyota has been flat for the past three years,” said Andrea. Toyota has been trending downward in the study on certain attributes, including technical and commercial knowledge. One underlying reason for the flatlining is the addition of new manufacturing plants. “It’s a growth churn,” Andrea said.

More From SAE Media Group

Automotive Engineering

Toyota Tops 2021 OEM-Supplier Relations Study

Automotive Engineering

Toyota Scores the Top Spot Again in 2024 OEM-Supplier Survey

Automotive Engineering

WCX 2023: Software-Defined Vehicle Development an Ongoing Headache for Industry

Automotive Engineering

Japanese OEMs Tops at Involving Suppliers Early in Development Process, Says 2014 Study

Automotive Engineering

Preparing for the New, Faster EV Product Cadence

Automotive Engineering

Tenured Production CEO Leading VW’s U.S. Electrified Manufacturing Push

Automotive Engineering

Innovative ‘Afreecar’ Wins SAE’s 2021 Create the Future Design Award

Automotive Engineering

Toyota Tops 2020 OEM-Supplier Relations Study

Automotive Engineering

GM CEO Barra Promises $30K EV SUV by Fall 2023; Automated Driving by Mid-Decade

Automotive Engineering

Honda and Nissan Merger Plans Could Accelerate EV R&D

Automotive Engineering

All-Electric Nissan Ariya Handles Ultra-Cold Temps on Pole to Pole Trek

Automotive Engineering

Corvette Hybrid Development Defies GM’s All-Electric Mantra

Automotive Engineering

Engineering ‘Electron Guzzlers’

Off-Highway Engineering

A Bevy of Battery and Fuel-Cell Electric Truck Reveals

Automotive Engineering

Engineering a Marvel of a Maverick Hybrid Transmission

Automotive Engineering

Seeking More Traction in Budding EV Market, VW Adds AWD to ID.4

Off-Highway Engineering

Allison Builds a Testing Powerhouse

Automotive Engineering

Preparing for a Lumpy EV Transition

Automotive Engineering

GM Unveils 2024 Chevrolet Silverado EV

Automotive Engineering

2022 Hyundai Santa Cruz: A Truck by Any Other Name

Autonomous Vehicle Engineering

Amending the Automated-Driving ‘Constitution’

Automotive Engineering

2022 Toyota Tundra: V8 Out, Twin-Turbo Hybrid Takes Over

Automotive Engineering

Preview: SAE 2021 WCX

Automotive Engineering

WCX 2024: The Technologies That Will Define Future Mobility

Automotive Engineering

Bringing Back the Hot Hatch: 2023 Toyota GR Corolla

Automotive Engineering

Personnel Moves at Denso

Automotive Engineering

The Battle over EV Value-Add Has Begun

Off-Highway Engineering

Western Star Adds ‘Weight Sensitive’ 47X to Vocational Lineup

Automotive Engineering

Schaeffler Builds an E-Motor Powerhouse

Automotive Engineering

Acura TLX Is Honda’s New Body-Build Benchmark

Top Stories

NewsSensors/Data Acquisition

![]() Microvision Aquires Luminar, Plans Relationship Restoration, Multi-industry Push

Microvision Aquires Luminar, Plans Relationship Restoration, Multi-industry Push

INSIDERRF & Microwave Electronics

![]() A Next Generation Helmet System for Navy Pilots

A Next Generation Helmet System for Navy Pilots

INSIDERWeapons Systems

![]() New Raytheon and Lockheed Martin Agreements Expand Missile Defense Production

New Raytheon and Lockheed Martin Agreements Expand Missile Defense Production

NewsAutomotive

![]() Ford Announces 48-Volt Architecture for Future Electric Truck

Ford Announces 48-Volt Architecture for Future Electric Truck

INSIDERAerospace

![]() Active Strake System Cuts Cruise Drag, Boosts Flight Efficiency

Active Strake System Cuts Cruise Drag, Boosts Flight Efficiency

ArticlesTransportation

Webcasts

Aerospace

![]() Cooling a New Generation of Aerospace and Defense Embedded...

Cooling a New Generation of Aerospace and Defense Embedded...

Energy

![]() Battery Abuse Testing: Pushing to Failure

Battery Abuse Testing: Pushing to Failure

Power

![]() A FREE Two-Day Event Dedicated to Connected Mobility

A FREE Two-Day Event Dedicated to Connected Mobility

Automotive

![]() Quiet, Please: NVH Improvement Opportunities in the Early Design Cycle

Quiet, Please: NVH Improvement Opportunities in the Early Design Cycle

Electronics & Computers

![]() Advantages of Smart Power Distribution Unit Design for Automotive &...

Advantages of Smart Power Distribution Unit Design for Automotive &...

Unmanned Systems

![]() Sesame Solar's Nanogrid Tech Promises Major Gains in Drone Endurance

Sesame Solar's Nanogrid Tech Promises Major Gains in Drone Endurance