The End of the Beginning: Why the EV Market Will Overcome the Loss of Tax Credits

The U.S. EV industry’s foundations are more solid than they appear to the casual observer. EVs are here to stay, but how quickly they rise to dominance and who controls the global automotive market are active questions.

As federal support for electric vehicles (EVs) in the form of tax credits, fuel economy standards, and grant programs is taken away, the question bears asking: Is this the end of an era of explosive EV industry growth?

In reality, it’s simply the end of the beginning; market data at home and abroad, significant investment in existing infrastructure, and the industry’s central role in multiple interconnected industries prove that EVs are here to stay.

Market Data

Today, EVs’ share of the U.S. light-duty car market sits around 11 percent, approximately 10 times higher than 10 years ago. EVs passed one million sales in a year for the first time in 2023; the very next year, 1.8 million were sold. The numbers are on track to rise again in 2025.

Globally, the industry is growing even faster. EVs represent one in five new vehicles sold globally and are expected to rise to one in four by the end of the year. Prices, primarily driven by the cost of producing massive batteries, continue to fall sharply year after year as new and more efficient chemistries are developed, production processes are scaled up and refined, and competition grows.

Revoking tax credits and other EV incentives will undoubtedly affect the market. Experts predict a short-term drop in sales after the September 30 deadline, when tax credits — worth up to $7,500 for new passenger EVs, $4,000 for used EVs, and $40,000 for large commercial electric trucks — will expire seven years early, due to recent federal legislation. But this is more of a speed bump than the end of the road. U.S. market share for EVs is still projected to more than double from 11 percent today to 27 percent by 2030, even without the tax credits. This is significantly lower than the 40 percent market share predicted with tax credits in place, but still represents substantial growth.

As EV sticker prices equalize with those of internal combustion engine (ICE) vehicles, their lower cost to fuel and maintain will tilt the total cost of ownership more firmly in their favor. Combined with a rapidly expanding lineup of available options (currently at well over 200 models), increasing numbers of public charging stations (232,000 nationwide as of September 2025), and longer battery ranges than ever before, electrification will become common sense for larger segments of the population.

EV readiness ordinances and fleet electrification policies are also expanding nationwide, creating a local-level regulatory environment built for electric transportation while continuing to drive demand for new EVs. EV readiness ordinances increase access to public charging; they also lower the price of adapting our infrastructure to electrification — reducing total costs by up to 75 percent — by ensuring that all new construction and major renovations are wired to facilitate future EV charger installation. Fleet electrification policies, spread largely to comply with state or municipal emissions targets, have now been proven to save governments substantial sums of money.

Infrastructure Investments

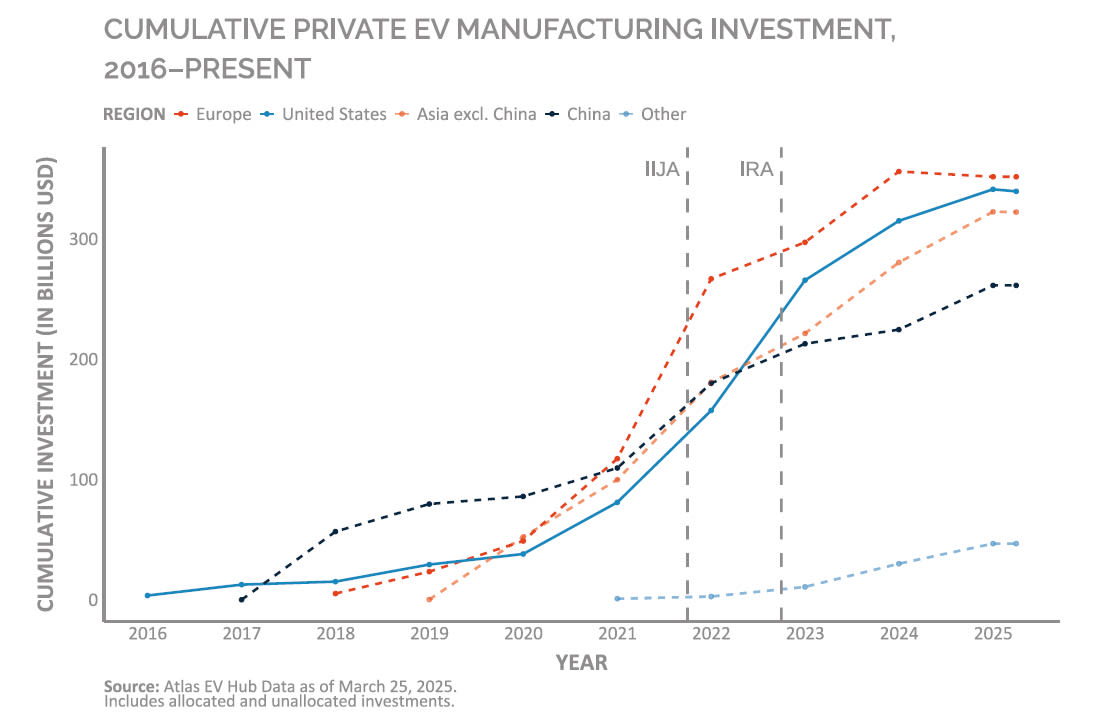

Hundreds of billions of dollars have already been invested in physical infrastructure and long-term electrification planning. These investments range from multibillion-dollar manufacturing facilities to entire workforce development pipelines formed between high schools, universities, and corporations. With domestic and global EV demand expected to rise significantly in the coming years, there is a near-guaranteed market for the talent and material outputs of these economic engines.

As highlighted so clearly by Ford’s assembly line-induced dominance over the global auto market in the early 1900s, the auto industry is ruled by efficiency and scale. For years, this fact incentivized automakers to postpone entering the EV market, but we’re quickly approaching the inflection point where sales figures and the state of existing infrastructure favor discontinuing ICE vehicle assembly lines in favor of a strategy of all-out electrification.

Ford’s “New Model T Moment” exemplifies this point perfectly, as does GM’s Ultium Cells program. Both automakers have committed to a long-term, affordability-centered vision of an electric transportation future and are dedicating themselves to maximizing the efficiency, scale, and output of their EV and battery manufacturing supply chains.

Local governments are working with high schools and universities to partner with corporations all along the EV and battery supply chains, forming programs that are already training an entire generation of workers for well-paid white-and blue-collar jobs as electricians, EV and charging software engineers, battery scientists, and positions mining and processing critical minerals. Georgia’s Quick Start program, City of Philadelphia’s Plug-In Philly, and the University of Nevada’s Nevada Tech Hub are prime examples.

Catalyzed largely by incentives introduced by the 2021 Infrastructure Investment and Jobs Act (IIJA) and 2022 Inflation Reduction Act (IRA), many of these investments and workforce development pipelines have come online recently or are expected to soon. Until recently, U.S. automakers have been forced to rely heavily on foreign expertise and easily disturbed Chinese supply chains. Powered by increasingly domestic expertise, labor, and materials, the future of the U.S. EV industry is more in our control than ever before.

EV and battery manufacturing and workforce development are not the only recipients of large-scale EV investment; nearly a quarter of a million public charging ports have already been installed across the country, with an average of more than 2,000 new ports added each month since the beginning of 2021. This expansion has continued unabated despite recent policy shifts, improving the EV ownership experience and reducing that prime driver of EV hesitancy: range anxiety.

Trends in Advanced Manufacturing

Strong enough to stand on its own, the EV industry’s centrality to wider trends in advanced manufacturing further strengthens its position. Critical minerals used to produce semiconductors and batteries now power an ever-increasing percentage of the world’s most advanced technologies, making their supply a central geopolitical aim. A brief overview of critical-mineral-dependent technologies includes military tech like drones, fighter jets, and advanced detection systems; renewable energy infrastructure like solar panels and wind turbines; the processors that enable AI models, and so much more.

And yet, despite the economic and security importance of these technologies, the EV and battery supply chains essentially determine the global flow of critical minerals. The EV and battery markets are far and away the biggest drivers of demand for these materials, and, therefore, the only industries capable of supporting the highly specialized mining, refining, and manufacturing processes their production requires. For the U.S. to ensure that it retains unrestricted and affordable access to these materials — and the technologies they enable — it must maintain a robust domestic EV industry.

New Frontiers for Electrification

EV manufacturing has also driven the revolution in battery technology that reduced the cost per kilowatt-hour (kWh) of battery production by 90 percent in 15 years, enabled the possibility of grid-scale energy storage, and now supports the 24/7 operation of many AI data centers. As the first generation of mass-market EVs is retired, an influx of still-functional, dirt-cheap batteries will enter the market, creating new opportunities for a wide range of non-vehicle second-life applications. Up to 95 percent of an EV battery’s inputs can be recycled using existing processes, so battery recycling is also taking off as its own industry.

While used EV batteries are already being repurposed to support the grid, an increasing number of EV batteries don’t have to wait that long to gain other uses; emerging vehicle-to-grid (V2G) technology that allows EVs to both give and receive power is also being deployed on ever-larger scales. School districts are using parked school buses to stabilize the local grid during periods of high demand, and people are using their own vehicles to provide life-saving power to their homes during extremeweather events.

Autonomous driving technology, which continues to improve and expand, is integrated far more easily into EVs than ICE vehicles and has a greater capacity to take advantage of EVs’ lower fuel costs. Rideshare drivers, who drive far more than most and represent a growing portion of the nation’s total miles traveled, also take advantage of EVs’ fuel savings more effectively than most.

Owners and operators of medium- and heavy-duty fleets with less efficient vehicles that often accumulate more miles than passenger vehicles may have the most to save through EVs’ lower cost of ownership. As the upfront costs of MHD vehicles — also primarily driven by the cost of batteries — decline, freight carriers and other high-mileage markets are heavily incentivized to electrify.

Conclusion

Losing billions in federal support will slow, but not stop, the growth of the U.S. EV market. All economic, infrastructural, and technological trends indicate that the EV industry is here to stay, so the right question is not whether the EV industry will survive, but how it will thrive.

Will EV sales in the U.S. double by the end of the decade, or more? Will the U.S. keep pace with China’s relentless iterative improvements on EV technology, or will China increasingly dominate the rapidly electrifying global transportation industry? Nobody knows the answers to these questions, but it’s clear that policy and industry need to work together to advance transportation electrification and strengthen U.S. economic and national security.

This article was written by Matt Stephens-Rich, Director of Programs, and Liam Condon, Senior Communications Associate, both at the Electrification Coalition (Washington, D. C). For more information, visit here .

More From SAE Media Group

Power Electronics INSIDER

Electric Vehicles Play a Surprising Role in Supporting Grid Resiliency

Battery & Electrification Technology

Solving Fleet Electrification Bottlenecks with Battery-Integrated Charging Systems

Battery & Electrification Technology

Battery Innovation Key for Commercial and Off-Highway EVs

Tech Briefs

Repurposing Mines for Underground Energy Storage

Battery & Electrification Technology

Advancing Battery Technology: The 2022 Battery Show Preview

Battery & Electrification Technology

New Products

Battery & Electrification Technology

Algorithms to Enhance Reliability of Electric Vehicle Charging

Battery & Electrification Technology

Advancing Battery Technology: The 2023 Battery Show Preview

Tech Briefs

Charging EVs as they Travel on Highways

Aerospace & Defense Tech Briefs

Delivering Operational Energy to Enhance Warfighter Capability

Power Management INSIDER

Used Nissan LEAF Batteries Given “Second Life”

Tech Briefs

Turning Coal Waste into a Resource for Clean EVs

Power Electronics INSIDER

Smart Grid for Stable, Reliable Electricity Supply

Power Electronics INSIDER

New Smart Charger May Pave the Way for More EVs

Off-Highway Engineering

Thor Lets Campers Go Further Off Grid With Electric Embark RV

Automotive Engineering

Rethinking the Grid for EVs

Tech Briefs

Real-Time Data for Smart Electric Mobility

Battery & Electrification Technology

Laying the Building Blocks for the EV Smart Grid

Power Electronics INSIDER

Reused car batteries rev up electric grid

Battery Technology

Advancing Battery Technology: THE 2021 BATTERY SHOW Preview

Tech Briefs

What is Intelligent Charging?

Top Stories

INSIDERManufacturing & Prototyping

![]() How Airbus is Using w-DED to 3D Print Larger Titanium Airplane Parts

How Airbus is Using w-DED to 3D Print Larger Titanium Airplane Parts

INSIDERManned Systems

![]() FAA to Replace Aging Network of Ground-Based Radars

FAA to Replace Aging Network of Ground-Based Radars

NewsTransportation

![]() CES 2026: Bosch is Ready to Bring AI to Your (Likely ICE-powered) Vehicle

CES 2026: Bosch is Ready to Bring AI to Your (Likely ICE-powered) Vehicle

NewsSoftware

![]() Accelerating Down the Road to Autonomy

Accelerating Down the Road to Autonomy

EditorialDesign

![]() DarkSky One Wants to Make the World a Darker Place

DarkSky One Wants to Make the World a Darker Place

INSIDERMaterials

![]() Can This Self-Healing Composite Make Airplane and Spacecraft Components Last...

Can This Self-Healing Composite Make Airplane and Spacecraft Components Last...

Webcasts

Defense

![]() How Sift's Unified Observability Platform Accelerates Drone Innovation

How Sift's Unified Observability Platform Accelerates Drone Innovation

Automotive

![]() E/E Architecture Redefined: Building Smarter, Safer, and Scalable...

E/E Architecture Redefined: Building Smarter, Safer, and Scalable...

Power

![]() Hydrogen Engines Are Heating Up for Heavy Duty

Hydrogen Engines Are Heating Up for Heavy Duty

Electronics & Computers

![]() Advantages of Smart Power Distribution Unit Design for Automotive...

Advantages of Smart Power Distribution Unit Design for Automotive...

Unmanned Systems

![]() Quiet, Please: NVH Improvement Opportunities in the Early Design...

Quiet, Please: NVH Improvement Opportunities in the Early Design...